The Australian Restructuring Insolvency and Turnaround Association (ARITA), with the help of professional services firm PricewaterhouseCoopers Australia (PWC), has published a tax guidance checklist to assist insolvency practitioners with identifying tax issues and their obligations on taking insolvency appointments. (Publication date 10 June 2015)

The checklist has 57 questions, alerts, recommendations and tasks concerning income tax, goods and services tax, fringe benefits tax, PAYG withholding, and superannuation guarantee.

ARITA suggests that “Members should note that while ARITA will endeavour to ensure that this guidance is kept up to date, tax is an area subject to constant change and the guidance is current, to the best of our knowledge, as at the date included in the footer of the document. Members should ensure that they are always using the most current version of the guidance”.

The checklist is intended to provide assistance and help to insolvency practitioners in the complicated field of tax compliance. There is no suggestion from ARITA that use of their tax guide is mandatory or necessary or even recommended.

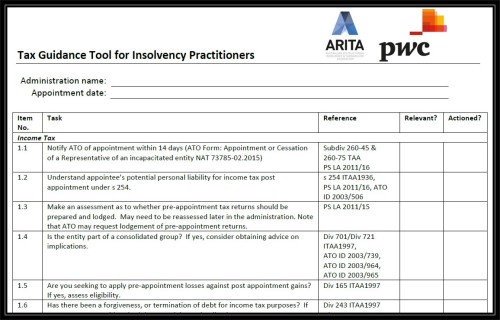

Extract from ARITA tax guide

Access to the full guide is available through the ARITA website: CLICK HERE.

Update 14 July 2015:

From ARITA on 13 July:

ARITA has received a number of queries from members regard the relevant PAYG Withholding Rates for dividends paid to employees by external administrators in light of the increase to the Medicare Levy.

On consultation with the ATO, we have been advised that the 2005 Notice of Variation is still current and the 31.5% standard rate still applies and will continue to do so until the notice of variation ceases on 1 October 2015.

The ATO further advises that it is looking to renew the notice but before that occurs will consult with relevant stakeholders, including ARITA and external administrators, about whether changes need to or should be made to the current notice, including any changes to the rates on the notice.