(Judgment of December 2015)

By a majority of three to two the High Court dismissed the Australian Taxation Office’s appeal in the Australian Building Systems case: Commissioner of Taxation v Australian Building Systems Pty Ltd (In Liquidation); Commissioner of Taxation v Muller and Dunn as Liquidators of Australian Building Systems Pty Ltd (In Liquidation) [2015] HCA 48 (10 December 2015) .

This test case – run by the Australian Restructuring Insolvency & Turnaround Association (ARITA) and the Australian Taxation Office (ATO) – began in 2013 and has previously been before the Federal Court and the Federal Court of Appeal. It was supposed to settle a far-reaching, long-standing argument that ARITA and the ATO had been having since 2009.

Argument about when obligation arises

The primary argument in this case – framed here as an issue for liquidators in general – has been whether the “retention obligation” placed on liquidators by section 254(1)(d) of the Income Tax Assessment Act 1936 arises prior to the issue of a tax assessment or only after the issue of an assessment.

The “retention obligation” is part of a provision that imposes an obligation upon agents and trustees (which includes liquidators) to “be answerable as taxpayer for the doing of all such things as are required to be done by virtue of this Act in respect of the income, or any profits or gains of a capital nature, derived by him or her in his or her representative capacity, or derived by the principal by virtue of his or her agency, and for the payment of tax thereon.” It states that an agent/trustee is:

“authorized and required to retain from time to time out of any money which comes to him or her in his or her representative capacity so much as is sufficient to pay tax which is or will become due in respect of the income, profits or gains”.

Personal liability of agent and trustee

For reasons which will become apparent later, it is important to note that under s.254(1)(e) the agent or trustee is “personally liable for the tax payable in respect of the income, profits or gains to the extent of any amount that he or she has retained, or should have retained …”.

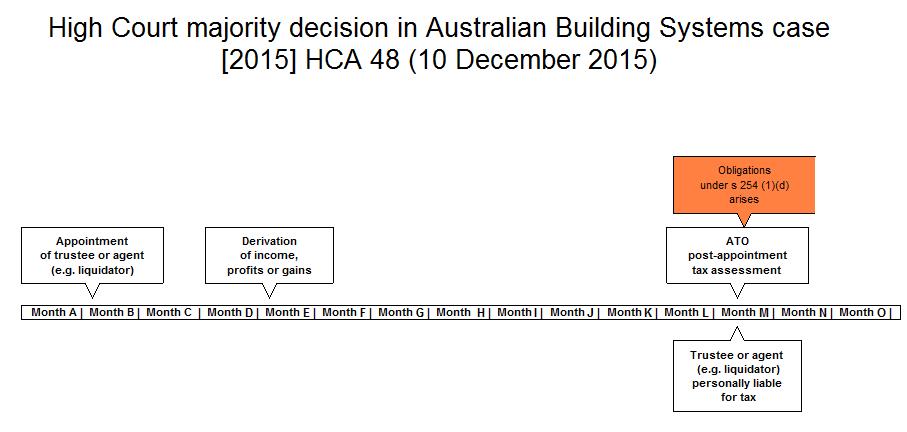

Majority decision

The majority of High Court judges held that obligations under s 254(1)(d) only arise after an assessment or deemed assessment has been made in respect of the relevant income, profits or gains. The following timeline chart illustrates their decision:

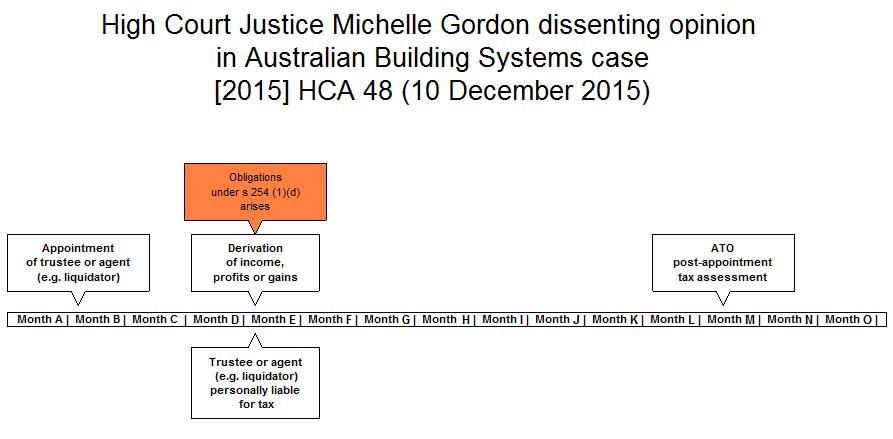

Dissenting opinion

Justice Michelle Gordon of the High Court

But one of the two dissenting judges – Justice Michelle Gordon – is of the view that the obligations under s 254(1)(d) do not depend on there being an assessment issued by the ATO. In her reasons Her Honour wrote of the “absurd results” that the majority’s construction of s 254 “leads to or at least has the capacity to lead to”; of how the majority’s construction of s 254 “is inconsistent with the evident purpose of the provision because it would leave the agent or trustee vulnerable between the time of derivation of the income, profits or gains and the time of assessment”; and of how the majority’s construction of s 254 “also ignores reality”.

Her Honour’s broad contrary view is illustrated in the next timeline chart. That is followed by another timeline chart illustrating how the “absurd results” and inconsistencies that she describes in her reasons arise.

Absurdities, inconsistencies and reality ignored

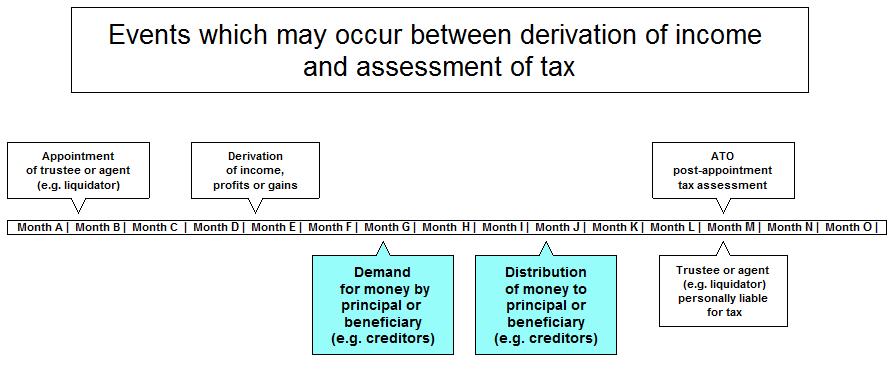

To illustrate the reasons for Her Honour’s criticism of the majority view, I begin by inserting into the broad timeline chart two events that may occur before a tax assessment is made.

(A third event – finalising a liquidation – may also occur before an assessment is made: see Her Honour’s “ignores reality” quote later in this blog.)

As can be seen, if the obligations under s. 254(1)(d) arise AFTER funds are distributed, the agent or trustee (e.g. the liquidator) probably won’t have any of the principal’s funds (e.g. company funds) with which to pay the tax. Justice Gordan said (at para. 214):

… (the majority’s construction of s 254 ) would leave the agent or trustee vulnerable between the time of derivation of the income, profits or gains and the time of assessment to claims by the principal or beneficiary for payment over of that income or those profits or gains, thereby denying the agent or trustee the means to pay the tax in respect of that income or those profits or gains. That denial of means to pay would directly conflict with, and contradict, the statutory direction in s 254(1)(a) and (b) that the agent or trustee is answerable as taxpayer in respect of that income or those profits or gains and for payment of the tax thereon.

Her Honour’s view is that the agent or trustee may be denied the means of paying the tax because without the retention authorization and obligation that s 254(1)(d) grants and imposes, it may be unlawful for the agent or trustee to retain funds. Her Honour said (at para 192):

Absent s 254(1)(d), there may be some argument about whether the retention by the agent or trustee of money belonging to another (an estate, a principal or a company), in the face of a demand from that person or entity, would be unlawful. On any view, s 254(1)(d) puts the matter beyond argument. Subject to important limitations contained within other sub-sections of s 254, s 254(1)(d) intersects with, and interrupts, any instruction to the agent or trustee for delivery up of money belonging to a beneficiary, a principal or a company and held by that agent or trustee.

Later, writing of “absurd results”, Her Honour said (at para 215):

… The effect of accepting that the retention authorization and obligation under s 254(1)(d) only arises after assessment would be that in many cases the income, profits or gains that would generate the tax liability will have been distributed by the agent or trustee before the obligation to pay the tax arises….

Then, in claiming that the majority view “ignores reality”, Her Honour spoke about the process of lodging tax returns (paras 216 and 217):

…. the assessment process is now one of self-assessment – generally a system where the Commissioner is taken to have made, on the day the return is filed, an assessment of the relevant taxable income or net income and of the tax payable on that taxable income or net income, being the amounts as specified in the return. It would be an odd result that a trustee (including a liquidator) could meet their obligations (under both the revenue law and the general law) to prepare a return for filing by way of self-assessment, recognise that tax is payable on the income, profits or gains derived by them in their representative capacity, but then distribute the funds sufficient to pay that tax immediately before filing the return…. Second, the contrary construction ignores the fact that a liquidation effectively comes to an end when the liquidator has realised and distributed all the company’s available property and made their report to the Australian Securities and Investments Commission. In many liquidations, that occurs relatively quickly and without the need for the company in liquidation to file an income tax return. In those cases, on the construction contended for by the Liquidators, the obligation to retain would never arise because a return would not be lodged and a deemed assessment would never be raised. Such a result is contrary to the express terms of s 254.

Corporations law

Although the Australian Building Systems case focused on provisions in the Income Tax Assessment Act, Her Honour devoted a significant part of her judgment to analysing the relevant duties and obligations of a trustee and a liquidator under the general law and corporate insolvency laws (paras 199 to 209).

Section 556(1) of the Corporations Act lists several debts which must be paid in priority to all other unsecured debts and claims. In Her Honour’s view (para 207):

A tax expense is an expense incurred by a liquidator. A tax expense may fall within s 556(1)(a) (an expense incurred in preserving, realising or getting in property of the company, or in carrying on the company’s business) or s 556(1)(dd) (other expenses). It is … a reflection of, and consistent with, the statutory scheme under the Corporations Act that post-liquidation creditors are to be treated equally, “in priority to all other unsecured debts and claims” and paid in a particular order….

Referring to and drawing upon two judgments about the tax expenses incurred by a receiver and a liquidator, Her Honour said (para 209):

For those reasons, a liquidator’s duties under, and the priority of payments provided for in, the Corporations Act are consistent with the construction of s 254(1)(d) that has the retention authorization and obligation applying on and from derivation.

Back when this test case began in the Federal Court, a decision was sought not just in respect of s 254 of the ITAA but also on the question of whether the liquidators were obliged under corporations law to pay to the ATO the whole of any tax due by the company in priority to other creditors. Unfortunately the Court decided not to address this question, deeming it “unnecessary to answer in light of the conclusion reached ”. (The conclusion reached then was the same as the majority decision of the High Court in the case.) Nevertheless, the presiding Federal Court judge (Logan J) gave his opinion on what a prudent trustee/liquidator would do:

… in relation to income tax, the liquidator would at the very least be entitled to retain the gain until the income tax position in respect of the tax year in which the CGT event had occurred had become certain by the issuing of an assessment or other advice from the Commissioner that, for example, no tax was payable in respect of that income year….”

Aside from that of Her Honour Justice Gordon, there appears to have been no further judicial opinion along these lines in subsequent judgments in this case. But Her Honour is, in effect, supporting Logan J’s cautionary advice by pointing out that such common sense and prudent behaviour is in keeping with the view that the statutory scheme of retention authorization and obligation created by s 254 is supposed to come into effect when income, profits or gains are derived.

The future

It remains to be seen whether Her Honour’s comprehensive, compelling, and extremely well-written analysis will result in a change to the legislation.

If not, perhaps the detrimental effects of the majority decision upon the ATO’s tax revenue collections will; for in this case $1.12 million in Capital Gains Tax was at stake.

Current ATO view

On 6 January 2016 the ATO issued a Decision Impact Statement concerning the High Court judgment. Under the heading “ATO View of Decision” the Statement says:

The Commissioner accepts that a trustee or agent has no obligation to retain under paragraph 254(1)(d) of the ITAA 1936 until an assessment has first issued in respect of the income, profits or gains.

The Commissioner will consider where it is now necessary to finalise draft taxation determinations TD 2012/D6 and TD 2012/D7. He will also consider the content of any revised Determinations.

The decision reflects the Commissioner’s view that section 254 of the ITAA 1936 does not require the trustee to be assessable to tax under Part III, Division 6 of the ITAA 1936 in order for the retention obligation to be imposed.

The decision also reflects the Commissioner’s view that section 254 of the ITAA 1936 is both an assessing and a collection provision.

The Commissioner agrees with the obiter comments made by Gordon J at [207] concerning the operation of section 556 of the Corporations Law, and will act accordingly.

It seems that although the ATO accepts the High Court’s majority decision (as, of course, it must), it’s interpretation of the decision is nuanced, and suggests that it has no intention of giving up on the retention obligation.

Previous blogs

My previous blogs on this subject:

► “Post-appointment income tax debts of liquidator” 10 October 2010

► “Taxing capital gains made during liquidation” 15 October 2010

► “Legal opinion warns external administrators about personal liability for company taxes” 16 November 2010

► “Insolvency Practitioners Assoc urges member caution on tax liability” 10 March 2011

► “Decision only partly resolves tax puzzle for liquidators” 7 March 2014

► “ATO appeals against decision in Australian Building Systems case” 19 March 2014

► “Tax Office wins right to appeal in test case regarding liquidators’ tax obligations” 27 April 2015

► “Tax Office loses High Court appeal in test case regarding liquidators’ tax obligations” 10 December 2015

Sorry, the comment form is closed at this time.