UPDATE TO THIS POST: In November 2016 the Treasury issued a revised proposal for consultation. See my blog titled “Levy on registered liquidators and other industries to help fund ASIC”.

A Government levy on registered liquidators is included in a draft proposal to adopt an “industry funding” model, or user-pays system, for the Australian Investments and Securities Commission (the ASIC). The levy is intended to recover costs incurred by the ASIC in regulating registered liquidators.

The Consultation Paper, issued on 28 August 2015, estimates that a flat levy on registered liquidators:

“… would equate to around $12,700 per year and some liquidators would potentially pay a high proportional fee relative to their costs of regulation.”

The paper discusses, as another option, the merits of the levy being based on “assets realised”. It states that one point in favour would be that:

“Levying liquidators on the basis of ‘assets realised’ would promote greater harmonisation between bankruptcy and corporate insolvency laws. It would be similar to the asset realisations charge administered by the Australian Financial Security Authority.”

In bankruptcies the liability to pay the asset realisations charge is that of the practitioner, but the amount of charge paid is borne by the estate or administration. This aspect is not discussed in the Consultation Paper. But presumably if the ASIC levy follows the bankruptcy scheme, the levy will be paid from funds held or realised by the company under external administration.

The Consultation Paper is titled “Proposed Industry Funding Model for the Australian Securities and Investments Commission”, and is available from The Treasury website. The proposal for registered liquidators begins at page 49 in “Attachment D – Funding Model for Registered Liquidators”. A copy of Attachment D appears below.

(Not all regulatory activities by ASIC are to be “funded by industry”. The paper states that: “The levies and fees-for-service proposed in this consultation paper do not recover the costs of …. the administration of the Assetless Administration Fund, which is used to finance preliminary investigations and reports by liquidators into the failure of companies with few or no assets where ASIC considers that enforcement action may result from the investigation.”)

____________________________ Beginning of Attachment D ____________________________

Attachment D – Funding Model for Registered Liquidators

In 2016-17, the Government would recover around $9 million through a levy on registered liquidators. There are around 700 registered liquidators.

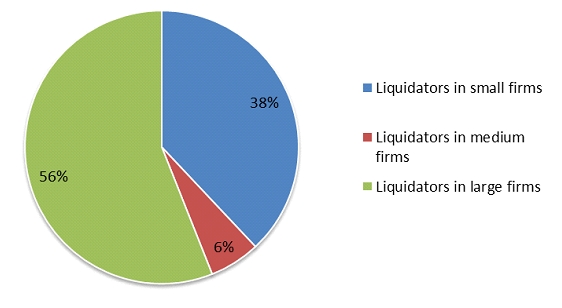

As at December 2014, 38 per cent of liquidators operated in small firms (involving one to four partners), 6 per cent operated within mid-sized firms (involving five to nine partners) and 56 per cent operated within larger firms with over ten partners. See Chart D1.

Chart D1: Distribution of registered liquidators

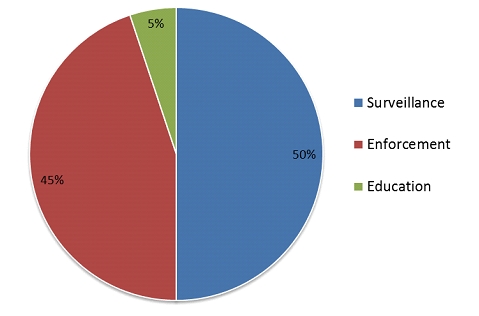

Registered liquidators are gatekeepers in the financial system and regulation works to ensure that liquidators fulfil their role diligently and transparently. Consequently, ASIC focuses on: competence; independence; and ensuring that liquidators do not improperly gain from their appointments.

To achieve this, ASIC:

- provides guidance to registered liquidators on ASIC’s expectations in relation to specific issues and behaviours;

- undertakes proactive risk-based surveillance, reactive surveillance, and compliance projects; and

- takes enforcement action to punish breaches of the law.

Chart D2 provides an overview of the activities expected to be undertaken for liquidators in 2016-17.

Chart D2: Forecast regulatory activities for registered liquidators

This consultation paper seeks views on recovering the costs of regulating registered liquidators through either a flat levy or another, more granular, methodology for calculating the annual levy. If Government introduced a flat levy, it would equate to around $12,700 per year and some liquidators would potentially pay a high proportional fee relative to their costs of regulation.

Alternatively, the Government could consider other methodologies for levying liquidators. Two metrics are proposed. These are:

- ‘assets realised’, calculated based on the total assets realised during the relevant period in an external administration; or

- the number of administration appointments (new and ongoing) undertaken each year.

Under both approaches, with the proposed levy payable in the forthcoming financial year calculated by reference to the liquidator’s activity in the current year, the levy payable will not precisely match ASIC’s costs of supervision in the forthcoming year. However, this approach would avoid the regulatory burden that up-to-date reporting would impose and reflects the fact that liquidators’ activity across years tends to be reasonably consistent.

Tiering on assets realised

Basing the levy for registered liquidators on ‘assets realised’ would be a good proxy for supervisory intensity. A registered liquidator who realises a higher value of assets each year either undertakes more external administrations or completes administrations with higher asset values. As a result, they generally present a larger risk and require more regulatory oversight.

Levying liquidators on the basis of ‘assets realised’ would promote greater harmonisation between bankruptcy and corporate insolvency laws. It would be similar to the asset realisations charge administered by the Australian Financial Security Authority.

Notwithstanding these benefits, for registered liquidators with sophisticated risk management systems adopting an ‘assets-realised’ methodology may result in levies that are higher than the relative cost of regulating them.

ASIC does not currently collect asset realisation data electronically. The annual electronic administration return proposed in the Insolvency Law Reform Bill 2014 could include asset realisation amounts.

Tiering on the number of external administration appointments

The number of external administration appointments undertaken reasonably predicts ASIC’s effort in regulating registered liquidators. That is, the more external administrations a registered liquidator undertakes, the more resources required to supervise that person.

However, for some registered liquidators, basing the levy on the number of appointments undertaken may not be a good proxy for supervisory intensity. For example, the levies payable are likely to be too low if the liquidator undertakes a low volume of appointments but each appointment has high asset values. In addition, due to the low volume of appointments, there is an increased risk that the firm’s procedures are not up to date and that the registered liquidator has not maintained their continuing professional education requirements. These factors lead to a higher regulatory risk.

In contrast, the levies would likely be proportionately high for liquidators that complete a large number of low value liquidations. In an extreme case, this could potentially result in a levy that exceeds their income from very low value liquidations.

| Questions:

1. Which of the potential levy arrangements for liquidators do you support? Why? 2. Would any of the proposed levy arrangements for registered liquidators not be competitively neutral? If so, why? 3. Would any of the proposed levy arrangements for registered liquidators not support small business? If so, why? 4. Would any of the proposed levy arrangements for registered liquidators not support access to liquidators in regional Australia? If not, why not? |

_____________________________ End of Attachment D ______________________________

Submissions

Interested parties are invited to comment on the proposed industry funding model for ASIC.

Closing date for submissions: Friday, 9 October 2015

Address written submissions to:

Senior Adviser

Financial System and Services Division

The Treasury

100 Market Street

Sydney NSW 2000Email: asicfunding@treasury.gov.au

For enquiries call Percy Bell (02) 6263 2048

Foreword to Consultation Paper

…. The Financial System Inquiry …. made a number of recommendations to strengthen the transparency, accountability and capabilities of our financial regulators. In the case of the Australian Securities and Investments Commission (ASIC), the Inquiry recommended that the Government should move to adopt an industry funding model, similar to that already in place for other Australian regulators….

(The Hon Josh Frydenberg MP Assistant Treasurer)

Context for Government’s consideration of an industry funding model

In 2014, the Financial System Inquiry found that ‘ASIC[’s] costs are not transparent to regulated industry participants’…. In response to these issues, the Financial System Inquiry recommended the introduction of an industry funding model for ASIC’s regulatory activities, in conjunction with enhanced accountability arrangements for ASIC. As proposed in this paper, ASIC would continue to be funded from the Commonwealth Budget, with a much larger share of its budget offset by charging industry levies and fees. Recovering a greater share of ASIC’s regulatory activities would be consistent with a number of comparable financial services and markets regulators in foreign jurisdictions where costs are recovered from industry …. This consultation paper seeks views on:

• the appropriateness of the proposed industry funding model;

• the costs and benefits of introducing an industry funding model for ASIC;

• the impact of the proposed model on competition and innovation; and

• the regulatory burden associated with the introduction of an industry funding model.

Benefits of an industry funding model for ASIC

Introducing an industry funding model for ASIC’s regulatory activities would:

1. ensure that costs are proportionately borne by those creating the need for regulation;

2. establish price signals to drive economic efficiencies in the way resources are allocated in ASIC; and

3. improve transparency and accountability.

END OF POST

Sorry, the comment form is closed at this time.