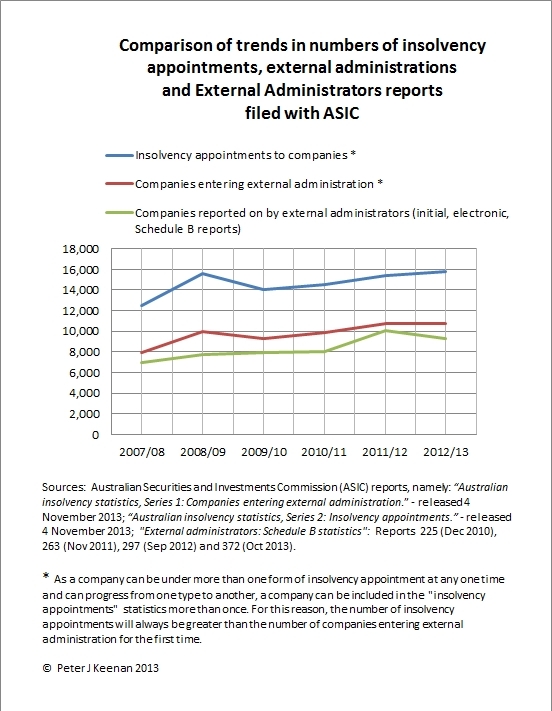

For the first time in six years the number of initial investigation reports filed with the Australian Securities and Investments Commission (ASIC) by external administrators has not risen in line with the increase in the number of companies entering external administration.

There could be several reasons for this variation, or it may simply be a blip. Next year’s statistics will be interesting.

The chart below, prepared exclusively for this blog using ASIC statistics, compares the trends from 2007/08 to 2012/13 in the numbers of corporate insolvency appointments, companies entering external administration and Schedule B investigation reports filed with ASIC.

ASIC does not appear to have commented publicly on the variation.

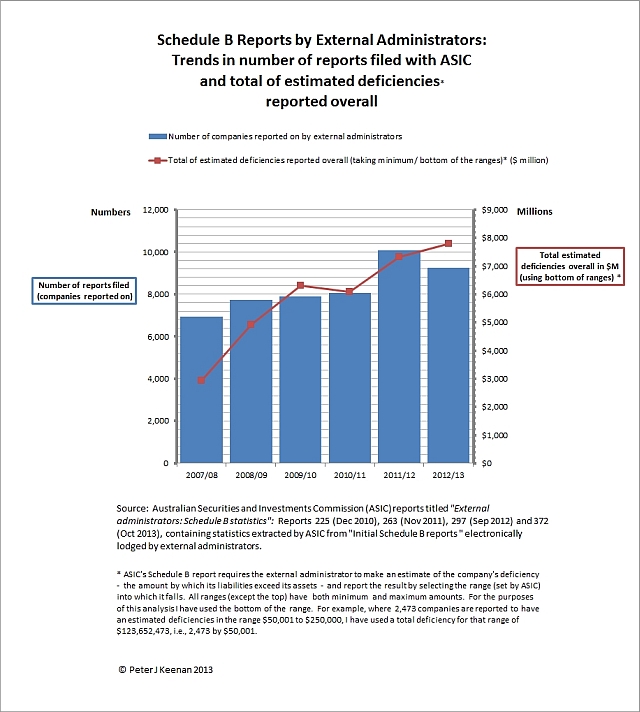

The following extracts from ASIC’s Report 372 (October 2013) give some general information about Schedule B reports:

“Liquidators, receivers and voluntary administrators (external administrators) must lodge reports under the following sections of the Corporations Act:

(a) s533 (by a liquidator);

(b) s422 (by a receiver); and

(c) s438D (by a voluntary administrator).

External administrators must lodge a report with ASIC as soon as practicable:

(a) when they suspect an offence under an Australian law, or instances of negligence or misconduct relating to the company to which they are appointed; or

(b) in the case of a liquidation only, when unsecured creditors are unlikely to receive more than 50 cents in the dollar dividend.

Changes to the Corporations Act introduced a statutory time limit on the lodgement of a s533(1) report by a liquidator appointed after 31 December 2007. A liquidator must lodge a report as soon as practicable and, in any event, within six months after it so appears to the liquidator that any of the conditions in s533(1)(a), (b) or (c) apply. No statutory time limit was introduced under s422 or 438D.”

…………………….

“The statistics in this report (on Schedule B investigation reports) do not directly correlate with the monthly statistics for ‘Companies entering external administration’ and ‘Insolvency appointments’ on ASIC’s website due to the time difference in lodgement of external administrators’ reports …. External administrators are not required to lodge reports where the pre-conditions of s422, 438D or 533 of the Corporations Act are not met.”