In the 2013–14 financial year, 7,218 reports alleging misconduct were lodged with ASIC by external administrators.

That’s one statistic contained in “Insolvency statistics: External administrators’ reports (July 2013 to June 2014)”, a report by the Australian Securities and Investments Commission (ASIC). The report (Report 412) is the latest data from ASIC on liquidations and other forms of external administrations.

ASIC Media Release

The following is from ASIC’s media release of 29 September 2014:

Report 412 Insolvency statistics: External administrators’ reports (July 2013 to June 2014) (REP 412) is ASIC’s sixth report and provides information on the nature of corporate insolvencies, supplementing the monthly and quarterly statistics that ASIC publishes on its website.

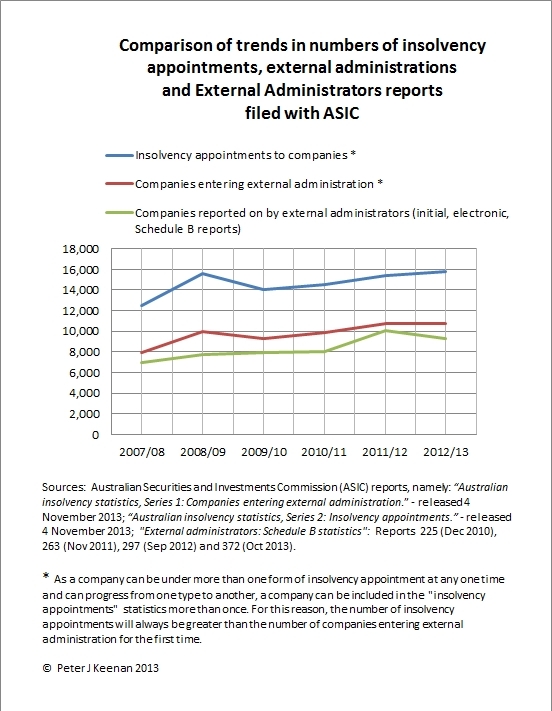

The report summarises information from 10,073 reports received during the 2013–14 financial year and includes ASIC’s response to reports of alleged misconduct from external administrators.

Commissioner John Price acknowledged the work of external administrators in carrying out their investigations and reporting to ASIC.

‘External administrators’ reports are a critical source of intelligence for ASIC. In addition to providing more detailed qualitative data, the information obtained from reports helps ASIC focus its regulatory efforts. It also helps us assess whether enforcement action is warranted, or if a director banning action should be pursued.

‘We encourage external administrators to provide these reports and any allegations of misconduct in a timely manner to assist in our supervision of insolvency and corporate governance issues,’ Mr Price said.

Profile of insolvent companies

REP 412 includes information about the profile of companies placed into external administration, including:

•industry types

•employee numbers

•causes of company failure

•estimated number and value of a company’s unsecured creditor debts, and

•estimated dividends to unsecured creditors.Table 1 summarises key data from the report.

REP 412 shows small to medium size corporate insolvencies again dominated external administrators’ reports. Of note, 86% had assets of $100,000 or less, 81% had less than 20 employees and 43% had liabilities of $250,000 (or less).

97% of creditors in this group received between 0–11 cents in the dollar, reflecting the asset/liability profile of small to medium size corporate insolvencies.

Allegations of misconduct

REP 412 details how often external administrators report alleged misconduct by company officers and the types of alleged misconduct most frequently reported.

In the 2013–14 financial year, 7,218 reports alleging misconduct were lodged with ASIC by external administrators.

ASIC asked external administrators to prepare 802 supplementary reports where external administrators alleged company officer misconduct. This accounted for 11.1% of all reports, which alleged misconduct, lodged in the financial year.

Supplementary reports are typically detailed, free-format reports, which set out the results of the external administrator’s inquiries and the evidence they have to support alleged offences. Generally, ASIC can determine whether to commence a formal investigation on the basis of a supplementary report. While only a portion of the offences reported may result in a formal investigation or surveillance, ASIC uses the information for broader intelligence and targeting purposes.

In both the 2012–13 and 2013–14 financial years, after assessment, ASIC referred 25% and 19% of these cases respectively for investigation or surveillance.ASIC considers a range of factors when deciding to investigate and take enforcement action and this is detailed in Information Sheet 151 ASIC’s approach to enforcement (INFO 151).

Future improvements: Reporting of alleged insolvent trading and other offences

To assist external administrators in their reporting obligations, ASIC anticipates releasing an amended report template for external administrators (Form EX01) in early-2015.

The amendments aim to capture more accurate information on alleged insolvent trading offences which might provide greater insight into the extent of insolvent trading and enable ASIC to focus our resources on matters that warrant further investigation.

The revised form is a further ASIC initiative to collect better information on corporate insolvencies in Australia. It complements recent enhancements to other forms to capture data in electronic format such as:

•industry statistics for external administration appointments from Form 505 (notice of appointment)

•key information from deeds of company arrangement from an enhanced Form 5047, and

•key financial data from Form 524 (presentation of accounts and statement).ASIC expects to continue our work with industry to improve reporting including on other offences, such as alleged breaches of director duties.

The full Report 412 is available for download in PDF format from ASIC.